Are you wondering what mortgage credit score you need to buy a house? Your credit score plays a key role in getting approved for a mortgage and securing the best loan terms.

But here’s the good news: there isn’t a one-size-fits-all number. Different loan types and lenders have different credit score requirements, and knowing these can save you time and stress. You’ll discover the credit score ranges that matter, how they affect your mortgage options, and what steps you can take to improve your chances of approval.

Keep reading to unlock the secrets that can bring you closer to owning your dream home.

Credit Score Basics

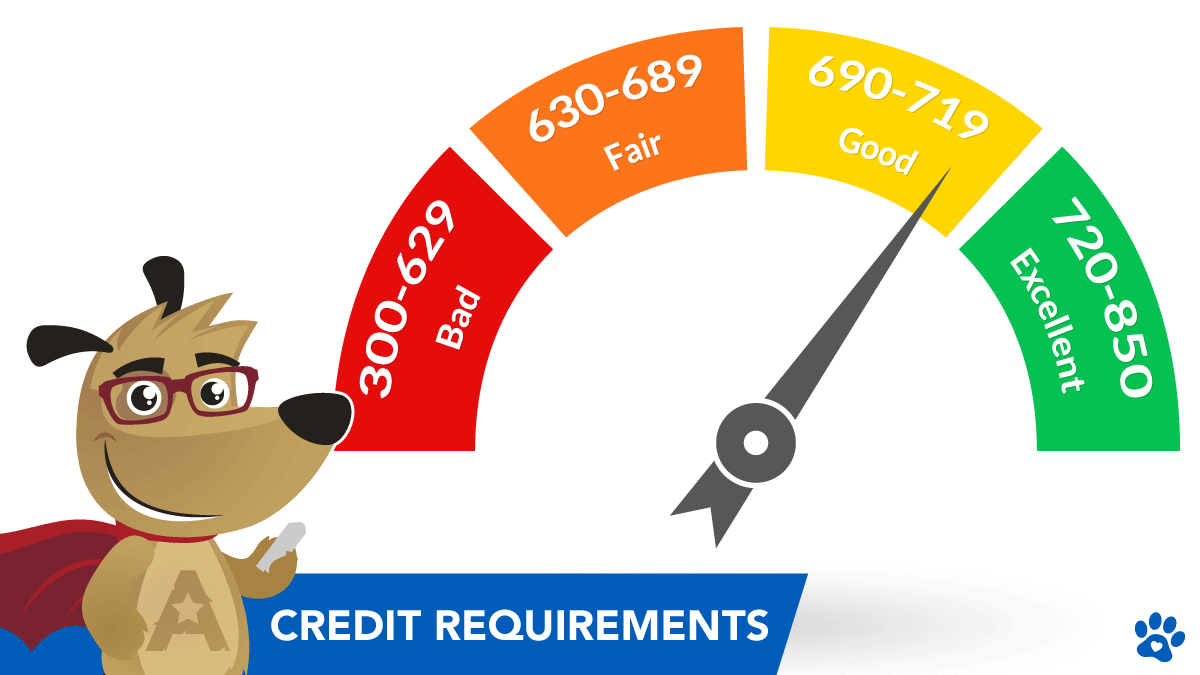

Credit scores show how well a person manages debt. Scores range from 300 to 850. A higher score means less risk to lenders. Scores are grouped into categories like poor, fair, good, and excellent. This helps lenders decide loan terms.

Mortgage lenders use credit scores to set interest rates and loan approval. Higher scores usually get better rates. Lower scores may mean higher rates or loan denial. Some loans need a minimum score, but options exist for lower scores too.

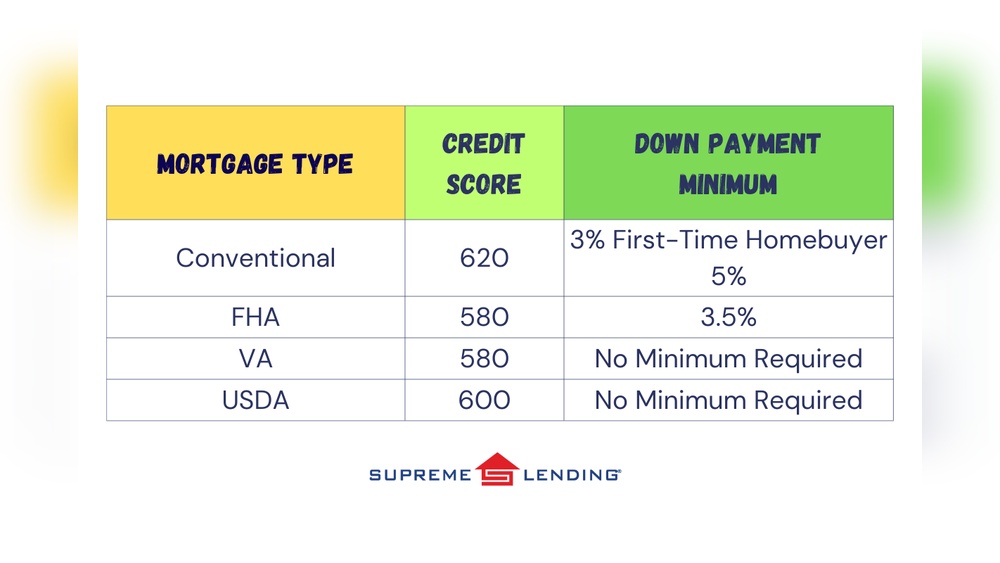

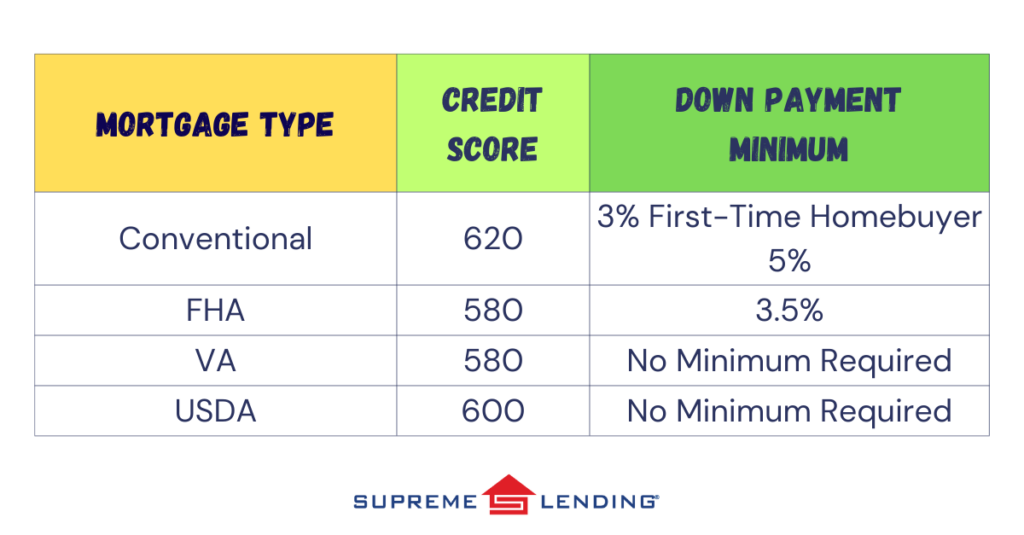

Score Requirements By Loan Type

Different loan types have different credit score needs. Conventional loans usually ask for a minimum score of 620. This helps lenders feel safe about lending money.

FHA loans are easier to get with a score as low as 580. Some lenders may accept scores between 500 and 579 with a bigger down payment.

VA and USDA loans often do not have a set minimum score. But most lenders like to see at least a 620 credit score. These loans help veterans and rural homebuyers.

| Loan Type | Minimum Credit Score |

|---|---|

| Conventional Loans | 620 |

| FHA Loans | 580 (can be lower with higher down payment) |

| VA and USDA Loans | No official minimum, usually 620 preferred |

Scores For First-time Buyers

Credit scores for first-time buyers usually fall into certain ranges. A good credit score typically starts at 620. Scores between 580 and 619 might still qualify for special loans. Scores under 580 can make it harder to get a mortgage. Different loan types require different scores. For example, FHA loans often accept scores as low as 500 with extra conditions.

Special programs exist to help buyers with lower scores. These include state and local programs offering down payment help. Some lenders offer low-credit or no-credit options. Veterans may use VA loans that have no minimum score requirement. USDA loans also help rural buyers with flexible credit rules.

| Loan Type | Minimum Credit Score | Notes |

|---|---|---|

| Conventional | 620 | Standard loans, best rates |

| FHA | 500 | With 10% down payment |

| VA | No minimum | For veterans and military |

| USDA | 640 | Rural areas, income limits |

Improving Your Credit Score

Pay bills on time to build a positive payment history. Keep credit card balances low, ideally below 30% of your limit. Avoid opening too many new accounts at once, as this can lower your score. Check your credit report regularly for errors and dispute them promptly. Use a mix of credit types like credit cards, loans, and mortgages to show responsible management. Maintain older accounts to help your score by increasing your credit history length.

Avoid missing payments, maxing out cards, and closing old accounts frequently. Beware of applying for too much credit in a short time. These actions can hurt your credit score. Stay patient—improving credit takes time and consistent effort.

No Money Down Mortgages

Zero down loan programs offer options for buyers with different credit scores. Minimum credit scores depend on the loan type chosen.

| Loan Program | Minimum Credit Score | Notes |

|---|---|---|

| USDA Loans | 640 | For rural areas, no down payment needed. |

| VA Loans | No minimum | Available to veterans, zero down required. |

| FHA Loans | 580 | Allows low down payment, sometimes as low as 3.5%. |

| Conventional Loans | 620+ | Some zero down options for first-time buyers. |

These programs help buyers with low savings or credit issues. Lenders look at credit scores to decide if a loan is safe. Scores below minimum might need extra proof of income or a co-signer.

Renting Vs Buying Credit Scores

Renting and buying a home require different credit score checks. Renting usually needs a lower credit score compared to buying. Landlords mostly check if tenants pay rent on time. They want to see a credit score around 600 or higher.

Mortgage lenders look at credit scores more strictly. Scores of 620 or above are often needed for good loan rates. Buying a home needs proof of steady income and low debt too.

Approval rules differ:

- Renting: Credit score, rental history, and income verification.

- Buying: Credit score, income, debts, employment, and savings.

Renting approval is quicker and less strict. Mortgage approval takes longer with more checks.

Using Score Calculators

Mortgage score calculators give a quick estimate of your eligibility. They use basic info like your credit score, income, and debts. These tools can help you understand what kind of mortgage you might get.

Accuracy varies. Some calculators use general rules, so results might not match real offers. They don’t check all details lenders consider, like employment history or savings.

Use them as a starting point. Check multiple calculators for a better idea. Remember, only a lender’s official review gives a final decision.

Frequently Asked Questions

What Credit Score Is Needed For A $400,000 Mortgage?

A credit score of at least 620 typically qualifies for a $400,000 mortgage. Higher scores improve loan terms and approval chances. Lenders may require 700+ for better rates. Exact requirements vary by lender and loan type.

How Rare Is An 830 Fico Score?

An 830 FICO score is very rare, ranking in the top 1% of all credit scores. It reflects excellent credit management.

What Is The 3 7 3 Rule For A Mortgage?

The 3-7-3 rule means refinancing a mortgage takes about 3 weeks, costs 7% of the loan amount, and saves money in 3 years.

How Much Do You Have To Earn To Qualify For A $200,000 Mortgage?

To qualify for a $200,000 mortgage, you generally need an annual income of $50,000 to $70,000. Lenders also consider credit score, debts, and down payment.

Conclusion

A good credit score helps you get better mortgage options. Different loans require different minimum scores. Lower scores may still qualify but with higher rates. Keep track of your credit and improve it when possible. This increases your chances of mortgage approval.

Understanding credit score needs makes home buying clearer. Take steps today to boost your credit health. Your dream home could be closer than you think.

Read More

- Credit Score Improvement Service: Boost Your Credit Fast Today

- Premium Credit Repair Consultation: Unlock Your Financial Freedom Today

- Travel Credit Card Comparison: Maximize Rewards & Save Big

- Low Credit Loan Approval: Quick Tips for Guaranteed Success

- Personal Loan Credit Requirements: Essential Tips to Qualify Fast

- Secured Credit Loan Options: Top Picks for Easy Approval

- Debt Consolidation Loan Rates: Unlock the Best Deals Today

- Credit Repair for Mortgage: Boost Your Score Fast & Secure Approval

- Credit Builder Loan Online: Boost Your Credit Score Fast

- Home Loan Credit Approval: Top Tips to Secure Your Dream Home