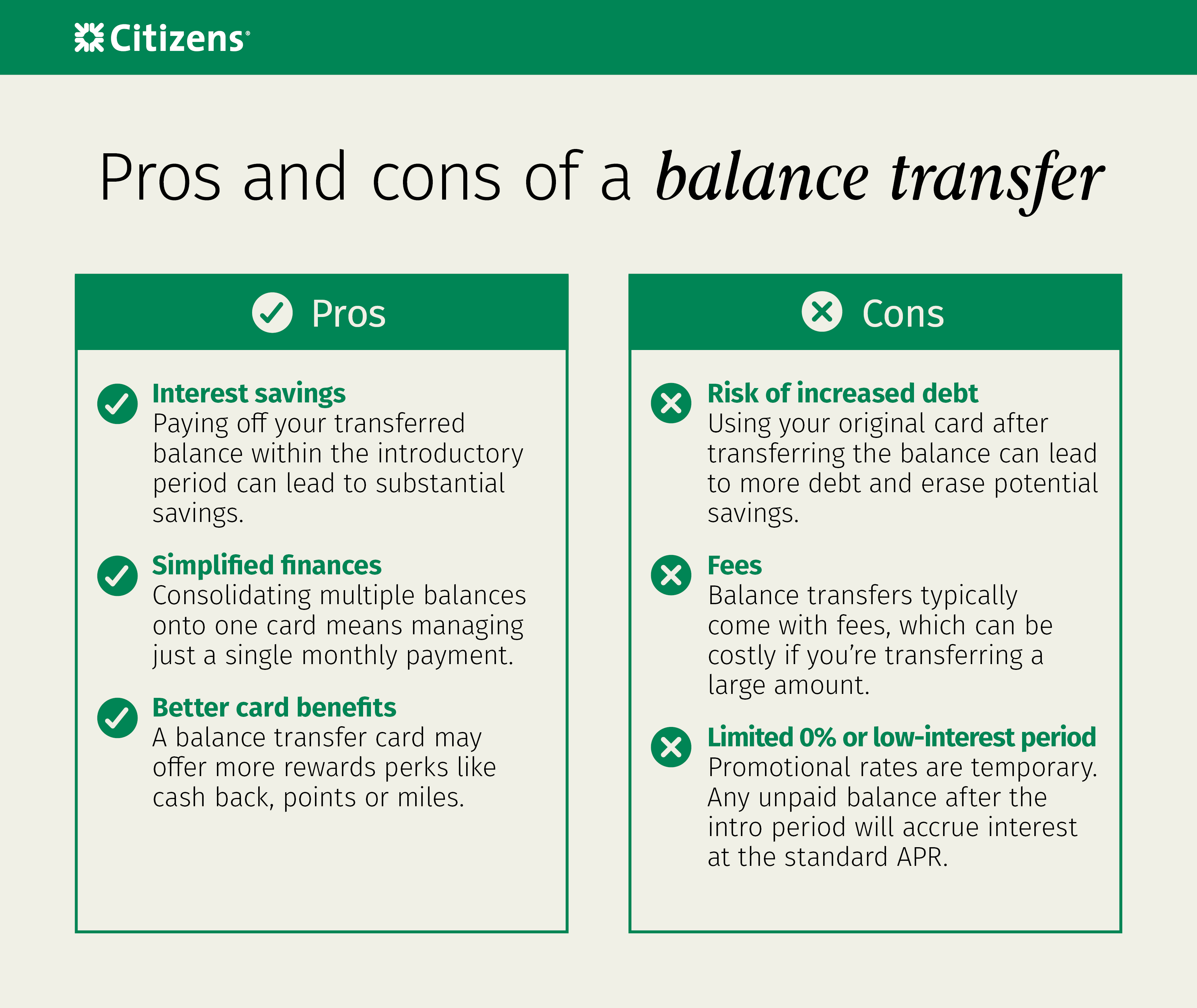

Struggling with high-interest credit card debt? A balance transfer card could be your secret weapon to save money and get back on track.

By moving your existing balances to a card with a low or 0% introductory APR, you can pause those costly interest charges and focus on paying down what you owe faster. But with so many balance transfer card offers out there, how do you choose the right one for your needs?

You’ll discover the best deals, key features to watch for, and smart tips to maximize your savings. Keep reading to take control of your debt and make your money work harder for you.

Top Balance Transfer Cards

Top balance transfer cards offer different benefits. The introductory APR period is how long you pay no interest on transferred balances. Some cards give 0% APR for 12 to 21 months. The balance transfer fee usually costs 3% to 5% of the amount transferred. A few cards have no transfer fee, which saves money.

Annual fees vary. Some cards have no annual fee, while others charge $95 or more. Cards with annual fees often have better benefits like travel perks or extra rewards.

Cash back and rewards make balance transfer cards more valuable. Some cards offer up to 1.5% to 2% cash back on purchases. Others give points or miles that can be used for travel or shopping.

| Card Name | Introductory APR Period | Balance Transfer Fee | Annual Fee | Best Feature |

|---|---|---|---|---|

| Wells Fargo Reflect® Card | Up to 21 months | 3% | $0 | Longest 0% APR period |

| Citi® Diamond Preferred® Card | 18 months | 3% | $0 | Good for balance transfers |

| Citi Double Cash® Card | 18 months | 3% | $0 | 1.5% cash back on all purchases |

| Chase Freedom Unlimited® | 15 months | 3% | $0 | Strong ongoing cash back |

How Balance Transfers Affect Credit

Balance transfers can affect your credit score in several ways. Moving a balance to a new card may reduce your credit utilization ratio, which often helps improve your score. This ratio is the amount of credit you use compared to your total available credit.

Paying on time during the promotional period is crucial. Late payments can lead to penalty rates and harm your payment history, which negatively impacts your credit score. The timing of your payments matters a lot.

Keep in mind, some cards may treat new purchases differently when you have a balance transfer. Interest might start accruing on new purchases immediately, so avoid extra spending until the balance is paid off.

Maximizing Balance Transfer Savings

Avoiding new purchases on your balance transfer card helps keep interest low. Many cards charge interest on new buys if you carry a transferred balance. This means paying more money each month.

Paying on time is key. Missing a payment may cancel your low introductory rate. It can also cause your interest rate to rise sharply. Set reminders to pay before the due date.

Choosing the right transfer amount matters too. Transfer only what you can pay off during the low-rate period. Too much can make it hard to clear your debt before rates increase.

Comparing Popular Card Offers

The Wells Fargo Reflect® Card offers a long introductory APR period with a low balance transfer fee. The Citi® Diamond Preferred® Card features a similar zero annual fee and a competitive introductory APR for balance transfers. With the Citi Double Cash® Card, you get a great balance transfer offer plus cash back rewards on purchases. The Chase Freedom Unlimited® card stands out for its strong ongoing cash back on everyday spending alongside balance transfer benefits.

| Card | Introductory APR Period | Balance Transfer Fee | Annual Fee | Best Feature |

|---|---|---|---|---|

| Wells Fargo Reflect® Card | Up to 21 months | 3% | $0 | Long intro APR period |

| Citi® Diamond Preferred® Card | Up to 18 months | 3% | $0 | Low fee balance transfer |

| Citi Double Cash® Card | 18 months | 3% | $0 | Cash back on purchases |

| Chase Freedom Unlimited® | 15 months | 3% | $0 | Strong cash back rewards |

Common Balance Transfer Fees

Balance transfer fees usually range from 3% to 5% of the transferred amount. Some cards charge a minimum fee, often between $30 and $50. For example, a 3% fee on $1,000 is $30, which matches a typical minimum.

These fees can reduce your overall savings. If the fee is too high, it may cancel out the benefit of a lower interest rate. Careful calculation helps decide if a balance transfer is worth it.

| Fee Type | Typical Range | Example |

|---|---|---|

| Balance Transfer Fee | 3% – 5% | $30 on $1,000 transfer |

| Minimum Fee | $30 – $50 | $30 minimum |

Applying For Balance Transfer Cards

Eligibility for balance transfer cards usually depends on your credit score and income. Most banks want applicants with a good or excellent credit history. They also check your current debts and payment behavior. Having a steady job and income helps your application.

Application tips include reading terms carefully. Check the introductory APR period and fees before applying. Fill out the form truthfully and provide all required documents. Applying online is faster and often easier. Avoid applying for many cards at once to protect your credit score.

Managing multiple transfers means keeping track of each due date. Pay on time to avoid penalty rates. Watch for transfer fees as they add to your balance. Try to focus on paying off one card at a time. This helps you reduce your debt faster and avoid confusion.

Alternatives To Balance Transfers

Personal loans offer a way to pay off credit card debt with fixed monthly payments. They often have lower interest rates than credit cards. This can make debt easier to manage.

Debt consolidation options combine multiple debts into one. This simplifies payments and may reduce interest rates. It helps people avoid juggling many bills each month.

Credit counseling services provide advice on managing money and debt. They can help create a budget and negotiate with creditors. These services support people in finding a clear path to financial health.

:max_bytes(150000):strip_icc()/Balance-transfer-fee_final-4a50b3eed4374262999696e1bb893ef9.png)

Where To Find Balance Transfer Deals

Bank websites provide direct, reliable information about balance transfer offers. You can see the latest rates, fees, and terms right from the source. These sites often have tools to help you compare offers and apply easily.

Comparison tools on finance sites let you view multiple cards side by side. This helps find the best introductory APR and lowest balance transfer fees. Many tools filter by fee, period length, or credit score needed.

Financial news sources often review and rank cards. They share tips on how to choose and use balance transfer offers wisely. Watching these can keep you updated on special promotions or changes in card terms.

Frequently Asked Questions

Do Balance Transfers Hurt Credit Score?

Balance transfers may cause a small, temporary dip in your credit score due to a hard inquiry and account changes. Maintaining timely payments helps protect your score.

Which Credit Card Offers The Best Balance Transfer?

The Wells Fargo Reflect® Card offers the best balance transfer with a long 0% APR period and no transfer fee. The Citi® Diamond Preferred® Card also provides excellent terms with no annual fee. Choose based on your transfer amount and repayment plan.

What Is The $750 Welcome Bonus Credit Card?

The $750 welcome bonus credit card offers a $750 reward after meeting spending requirements. It often includes perks and promotional APRs.

Who Has The Longest 0% Balance Transfer?

The Wells Fargo Reflect® Card offers the longest 0% balance transfer period, up to 21 months. It charges no annual fee and has a low transfer fee.

Conclusion

Balance transfer card offers can help you save on interest charges. Choose a card with a low or zero introductory APR. Watch out for balance transfer fees and how long the offer lasts. Make payments on time to keep the promotional rate.

Avoid new purchases while paying off transferred balances. Compare different cards to find the best fit for your needs. Using balance transfers wisely can reduce your debt faster. Plan carefully, and you can improve your financial health.

Read More

- Credit Score Improvement Service: Boost Your Credit Fast Today

- Premium Credit Repair Consultation: Unlock Your Financial Freedom Today

- Travel Credit Card Comparison: Maximize Rewards & Save Big

- Low Credit Loan Approval: Quick Tips for Guaranteed Success

- Personal Loan Credit Requirements: Essential Tips to Qualify Fast

- Mortgage Credit Score Needed: Unlock Homeownership Success Today

- Secured Credit Loan Options: Top Picks for Easy Approval

- Debt Consolidation Loan Rates: Unlock the Best Deals Today

- Credit Repair for Mortgage: Boost Your Score Fast & Secure Approval

- Credit Builder Loan Online: Boost Your Credit Score Fast